Start saving early and let compound interest grow your retirement nest egg

With the current debate surrounding the Government’s proposed changes to superannuation contributions caps focused on tax rather than outcomes, most super fund members should instead be concentrating on maximising their investment returns to achieve an adequate retirement income, according to Rice Warner research.1

The analysis demonstrates that a balance of $1.6 million (the Government’s new tax-free cap for pensions) can be achieved if the individual has the capacity and desire to save regularly from an early age while simultaneously letting compound interest do the rest of the heavy lifting.

In simple terms, compound interest is interest paid on the initial principal as well as the accumulated interest on money you have borrowed or invested. This means you earn interest on the money you deposit, and on the interest you have already earned - so you earn interest on interest.

For example, by doing so, a 25-year-old with no balance would only need concessional contributions of $20,300 per annum in order to achieve a balance at retirement of $1.6 million.1

You can reach $1.6 million if you start saving early

Rice Warner’s modelling shows that irrespective of the proposed changes from 1 July 2017, individual fund members can save at least $1.6 million (the proposed new cap on the balance members can have in the retirement phase of super where earnings are tax-free) in superannuation.

Specifically, it found that bringing contributions forward makes this goal more attainable.

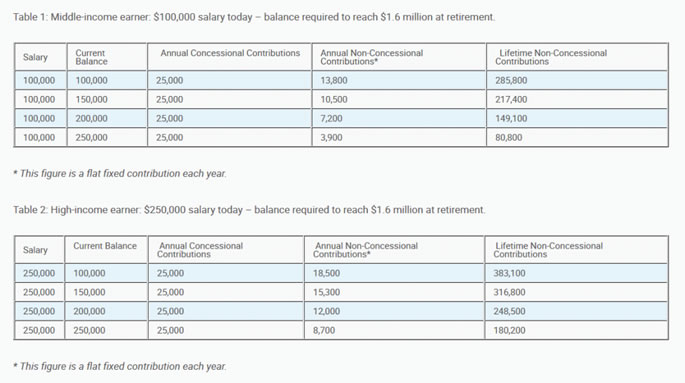

To illustrate this, and as set out in Table 1 and Table 2 (values in today’s dollars), Rice Warner prepared eight case studies of fund members aged 40 with an intention to retire at 67 (the future eligibility age for the Age Pension).

Four of the members are currently earning $100,000 a year with the other four earning $250,000 a year. Notably, the amount of tax paid on concessional contributions will be double for the higher income earners. Their existing superannuation balances range from $100,000 to $250,000.

Based on certain assumptions, including an annual (long-term) fund earning rate of 6.0% and wage inflation of 3.5%, Rice Warner calculates that all the fund members are able to reach the $1.6 million cap by retirement age.

However, in order to do this with conservative earnings of 6.0%, the members must fully utilise their concessional contributions cap and make non-concessional contributions which range from $4,000 per annum to $19,000 per annum, depending on their current financial situation.

Members with low balances who leave saving in superannuation to much later in life (such as post age 50) will struggle to accumulate a balance of $1.6 million by retirement.

Compound interest saves the day

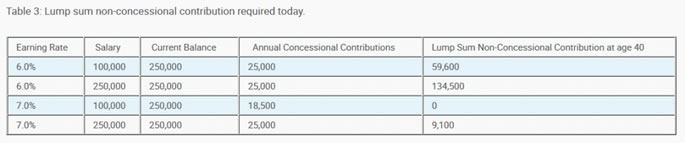

Rice Warner’s research also shows that the outcome for retirees is very sensitive to the assumed earnings rate. Table 3 (values in today’s dollars) demonstrates that if the earnings rate were 1% higher, it would eliminate most (if not all) of the need for non-concessional contributions for the two scenarios considered.

Assumptions: Fund earning rate 6.0%, CPI 2.0%, wage inflation 3.5%.

Additionally, if a member is able to make a significant one-off non-concessional contribution in the immediate term this can reduce their total non-concessional contributions burden by over 25%.

Therefore, according the Rice Warner analysis, the most effective approach is to start saving early and to let compound interest do the rest of the heavy lifting to get to $1.6 million.

However, in conclusion, Rice Warner concedes that while fund members with very high incomes would be able to achieve the levels of required contributions, this will remain out of reach for many.

Note:

- The Government’s proposed $1.6 million cap on pension accounts is indexed. Under Budget proposals, concessional contributions of more higher-income earners will become liable for Division 293 tax.

- Concessional contributions are subject to tax at 15%, and under the Budget proposal, from 1 July 2017 those earning over $250,000 in Adjusted Taxable Income will pay tax at a higher rate of 30%. Subsequently, for these members a contribution of $25,000 will only be $17,500 after tax.

1 Rice Warner’s website http://ricewarner.com/start-early-and-use-compound-interest-to-build-your-retirement-benefit/

Source: Colonial First State